Key Takeaways

- House prices are unlikely to go down on a national level, but they should grow more slowly.

- It’s normal for house prices to steadily rise over time—it’s actually abnormal when they fall and can signal a broader economic issue, like a recession or correction.

- Home prices surged during the pandemic as buyers took advantage of ultra-low mortgage rates, leaving prices elevated today.

- In a few Sun Belt cities like Austin and Nashville, prices are falling after the pandemic boom left them inflated.

It’s no secret that housing today is expensive. Home prices are nearly 50% higher than they were in 2020, while mortgage rates have almost doubled. A shortage of inventory, spike in inflation, and a surge in demand during the pandemic were the leading reasons, pricing many consumers out.

Thankfully, the housing market has begun leveling out, and economists say that affordability will improve over the next few years. House prices are unlikely to fall, but they should grow more slowly, helping wages catch up.

So, if you’re a homebuyer stuck on the sidelines wondering if house prices will ever go down, this article is for you. We’ll break down why prices are most likely not going to fall, why most economists believe affordability will still improve, and what buyers and sellers can do to win today.

From Redfin’s Chief Economist

“House prices aren’t going to fall on a national scale any time soon—and that’s actually a good thing. It’s normal for house prices to rise gradually over time, just as a mild inflation rate is healthy for most economies. The difference is when prices jump all at once like they did during the pandemic housing boom, which sidelined most buyers and sellers. Now, though, affordability is starting to increase because wages have been increasing faster than housing costs since late 2025. We expect this to continue for the foreseeable future.” – Daryl Fairweather, Redfin Chief Economist

Why are house prices so high?

The pandemic-era economy threw the housing market into overdrive before it fell back down to earth. One result of this was a surge in home prices, which have remained stubbornly elevated ever since—straining budgets and keeping many buyers and sellers on the sidelines. According to Redfin data, the typical homebuyer has had to spend well over 30% of their income on housing since March 2022.

Diving a bit deeper, though, there are three primary reasons why home prices are so high today: limited housing inventory, insufficient homebuilding, and volatile mortgage rates. Let’s break these down.

>> Read: Why Are Houses So Expensive?

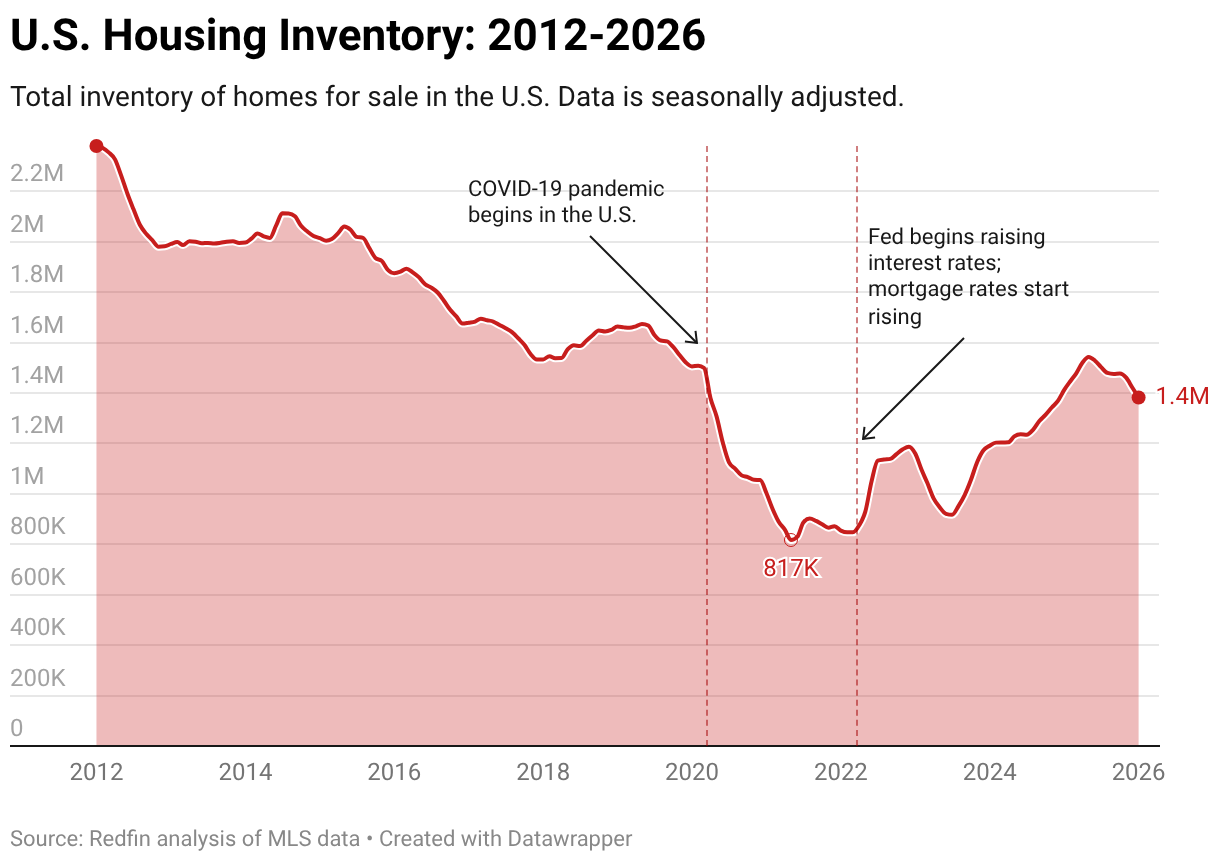

1. Limited housing inventory

America has a chronic housing shortage. Estimates range from between 1.5 to 7 million homes, with the shortage creeping up at the turn of the century and speeding up following the Great Recession.

When there aren’t enough homes for sale for people who want them, prices rise; when the shortage gets more severe, prices tend to increase even faster. That’s what’s been happening for the last 15 years—and especially the last five years.

When mortgage rates dropped to record lows during the pandemic, buyers took advantage of lower costs and bought up a large share of the available homes for sale. This depleted supply and pushed prices to record highs. The effect of this continues to linger.

Today, inventory is slowly improving, but the volatile and expensive economy is keeping substantial growth at bay. “It’s a pretty difficult pattern to break,” noted Fairweather. “High prices are making it less attractive for homeowners to list their homes for sale, which in turn keeps prices elevated because inventory remains low. A steady increase in new construction at price points consumers can afford is the best way to meaningfully bring costs down nationwide.”

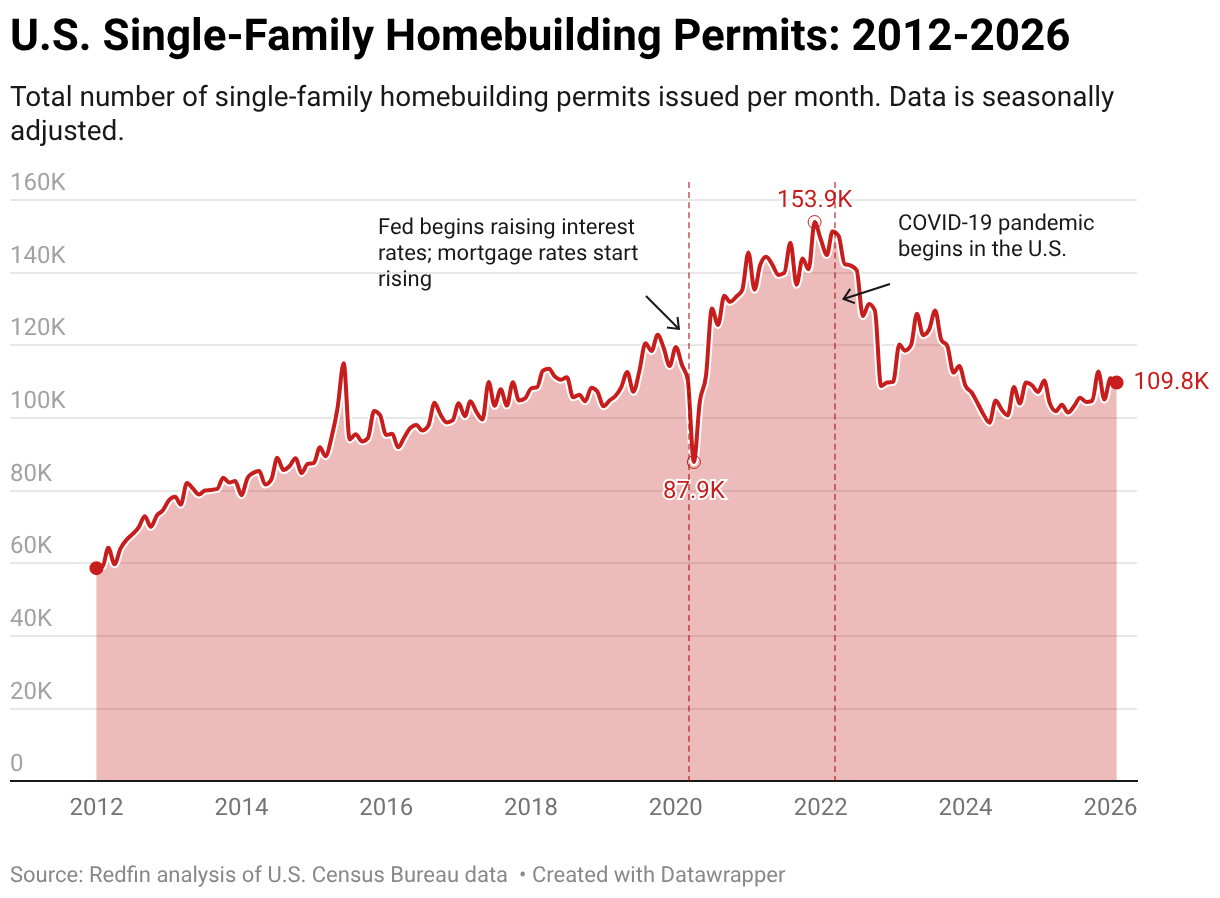

2. Insufficient homebuilding

The U.S. relies on a steady supply of new houses to support its growing population. Historically, this balance has been relatively stable, with construction booms and busts following wars or economic shocks. But ever since the Great Recession, homebuilding has severely lagged behind demand, meaning there isn’t enough new supply injected into the market. This is one reason why the typical house today is older than ever.

Homebuilding has ramped up since the pandemic, but more homeowners have to sell and more homebuilders have to build for the shortage to ease.

3. Volatile mortgage rates

Mortgage rates play an integral role in determining housing affordability. The higher the rate, the more expensive the monthly payment is for homebuyers. And when rates are lower, it’s generally more appealing to buy.

That’s what happened during the pandemic, when ultra-low rates incentivized homebuyers to buy a huge number of homes from 2020-2022, depleting inventory and helping prices swell. But that pattern flipped once rates jumped back up.

Now, the housing market is somewhat stuck, with mortgage rates relatively elevated and prices still high, keeping many buyers out of the market. But as time goes on and more people realize this is the new normal, it’s likely that more consumers will test the waters and look to buy or sell.

When will house prices go down?

Nationally, house prices are unlikely to go down anytime soon. The housing market is slowly recovering from the volatility over the last few years, and Redfin economists expect prices to grow more slowly moving forward.

“A more accurate question to ask would be ‘when will housing affordability improve?’,” said Fairweather. “And the answer is ‘right now!’ Wages are growing faster than housing costs, thanks to steadily declining mortgage rates and level house prices. We expect this to continue as the housing market undergoes a prolonged reset for the next few years.”

Outside of modest corrections or isolated drops, it’s generally not a good thing when home prices fall. If house prices were to go down, homeowners would lose equity, buyers may pull back out of fear that a crash was coming, and a broader economic shift would likely already be underway.

Across the broader economy, steady price growth paired with rising incomes is what economists view as a sign of a healthy, expanding economy. A mandate of the U.S. Federal Reserve System (the Fed) is to keep the inflation rate as close to 2% as possible. Shelter costs—i.e. home sale and rental costs—have an outsized impact on inflation; their pandemic-era spike is a reason why inflation remains above the Fed’s target.

Are house prices falling anywhere?

Today, house prices are falling primarily in the most popular pandemic-era migration destinations—cities like Austin, Nashville, and San Antonio. These cities saw large surges in population and buyer activity from 2021-2022, but have since fallen out of popularity as prices grew too high and remote work came to an end. Now, in many of these markets, there are far more sellers than buyers in these cities, pushing prices down.

Austin is a prime example. The Texas metro has flipped from the hottest major city in the nation to the coldest in the last three years. Prices have dropped by $150,000 from their peak, and the typical home takes more than 100 days to sell.

How do falling house prices affect homebuyers and sellers?

In most cases, waiting for home prices to drop may not be the best strategy. While prices may be falling in some markets, most economists expect them to grow slowly rather than decline nationwide. That means buyers who wait could miss opportunities to negotiate with sellers or lock in a home that fits their needs.

That said, falling prices can affect buyers and sellers differently.

For homebuyers

At first glance, falling house prices sound like a good thing for homebuyers; they now have to spend less for a home than they thought.

However, a drop in house prices is often the result of a larger economic shift—like a market correction or interest rate spike—which can actually make buying a home harder. Buyers may face challenges such as:

- Potentially higher mortgage rates

- Reduced purchasing power

- Greater job uncertainty

- Declining home values, which could make it harder to move in the future

Because of these factors, waiting for prices to fall doesn’t always work out the way buyers expect.

“If you’re a buyer waiting for prices to fall, you may want to rethink your strategy,” continued Fairweather. “More sellers are cutting prices to attract buyers, but only a few cities are actually seeing prices consistently drop—and buyers may not want to invest in a home that is losing value. In most parts of the country, though, now is actually a good time to buy, because competition is low and sellers are willing to negotiate.”

>> Read: Is Now a Good Time to Buy a House?

For home sellers

Falling house prices can be negative for homeowners and sellers for many reasons:

- Their homes are now worth less, since falling prices means declining value

- Lower prices often reflect—and can further reduce—buyer demand

- Buyers may be hesitant to purchase a home losing value

- Market uncertainty can make it harder to plan next moves, such as buying another home or relocating

Additionally, some homeowners may be forced to sell at a loss, especially those who bought during the pandemic peak and now want or need to move. A Redfin analysis from 2025 found that nearly 6% of sellers who bought a home from 2020-2022 were at risk of losing money on the sale.

“If home values are falling, that often means the market is resetting or economic volatility is running high—both bad news for sellers,” added Fairweather. “Most buyers may also be wary of making a risky investment, which could make it harder for sellers to close quickly. Thankfully, sellers today can expect home prices to climb slowly and demand to inch back in many markets as affordability improves.”

>> Read: Should I Sell My House Now?

Is the housing market crashing?

No, the housing market is not crashing—although it is slow, expensive, and has gone through a few turbulent years. A crash is generally the result of an economic or financial shock, like a recession, high inflation, or major labor market decline. Crashes often lead to a widespread decline in home prices, buyer activity, and a surge in foreclosures and loan delinquency.

Most economists agree that the housing market is not going to crash, either, but is instead undergoing a long-term correction that is already underway. House prices will climb slowly or fall in overheated markets, inventory will climb, and buyers will continue to have negotiating power until affordability improves enough for the balance to level out.

>> Read: Is the Housing Market Going to Crash?

Final thoughts: Prices are leveling out, but won’t drop anytime soon

House prices are most likely not going to go down in the near future but will instead return to more “normal” growth levels. There are a few places where prices are falling, but they are generally limited to cities in the Sun Belt that saw prices skyrocket to unsustainable levels and are now correcting.

Falling prices aren’t necessarily a good thing, either, since they can mean lower home values and are often the result of economic stress. A healthy, growing economy is one where prices and incomes rise slowly over time, keeping costs affordable and households able to maintain their purchasing power.

There is a lot of uncertainty today, from tariffs, to international conflicts, to AI fears and inflation worries. Economists believe the housing market is starting to stabilize.